Introduction

As we navigate the first quarter of 2026, the global Phosphate Rock price is facing a convergence of operational complexities and regional price shifts. For fertilizer producers and procurement managers, the period between February and April presents critical supply chain risks. This analysis explores why the coming months will be a testing time for the industry and how to navigate these challenges strategically.

1. Supply Bottlenecks in Major Hubs

The current market is primarily driven by a physical tightening of supply from the world’s largest exporters. Two major factors are at play:

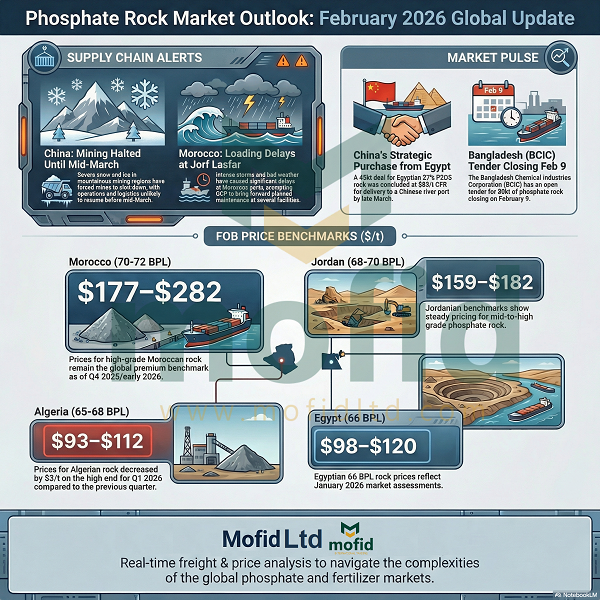

• Logistical Delays in Morocco: Bad weather has significantly disrupted operations at key Moroccan ports, including Jorf Lasfar. These delays have hindered OCP’s loading schedules, creating a ripple effect that reduces the availability of spot cargoes in the immediate term.

• Seasonal and Climatic Halts in China: While China remains a massive producer, most of its mines have shut down for the Lunar New Year holiday. More critically, heavy ice and snow in mountainous mining regions are expected to delay the resumption of full operations until mid-March. This removes a significant volume of rock from the international export window during a peak demand period.

2. Price Benchmarks: Stability vs. Strategic Opportunities

Global phosphate rock price is currently showing a “dual-track” behavior. While traditional high-grade hubs remain firm, new competitive windows are opening elsewhere:

• High-Grade Firmness: FOB prices for high-grade rock in Morocco (70-72 BPL) are holding steady between 282/t, while Jordanian (68-70 BPL) rock is assessed at 182/t.

• The Algerian Strategic Window: In a notable move, Algeria has decreased its 1Q 2026 prices by 93–$112/mt FOB. For buyers looking to optimize costs without sacrificing quality, this represents a golden opportunity.

• Competitive Egyptian Offers: Egyptian rock (66 BPL) continues to attract Asian buyers with prices ranging from 120/MT FOB, maintaining its position as one of the most cost-effective origins in the current market.

3. Strategic Maneuvers by Major Market Players

Sophisticated buyers are already moving to secure volumes ahead of the spring demand peak. China, despite its domestic capacity, recently purchased 45,000t of Egyptian rock at $83/t CFR to ensure inventory levels through the end of March.

Simultaneously, large-scale tenders, such as the 30,000 MT rock tender by BCIC Bangladesh closing on February 9, indicate a growing urgency among importers to lock in supplies before further volatility hits.

4. Production Costs and Margin Pressure

It is also vital to monitor the producers’ side. In China, high raw material costs (specifically sulphur) have pushed some domestic phosphate producers into losses of approximately $86/MT (Yn600/MT). This financial pressure often leads to reduced run rates or a shift toward more aggressive export pricing once export windows reopen to recoup losses.

Strategic Recommendation: Security of Supply Over Price Speculation

Given the port delays in North Africa and the weather-induced mining halts in East Asia, waiting for a significant price drop in March carries high operational risks.

At Mofid Ltd., our recommendation to partners is to prioritize “Supply Security.” Utilizing the current competitive pricing windows in Algeria and Egypt while closely monitoring freight rate fluctuations in the Red Sea is the most effective way to ensure production stability in the coming months.

——————————————————————————–

About the Author

This analysis was prepared by the CEO of Mofid Ltd. and a specialist in the global phosphate rock market. For tailored market reports, current price benchmarks across all grades, or procurement consulting, you can connect with him directly on LinkedIn: